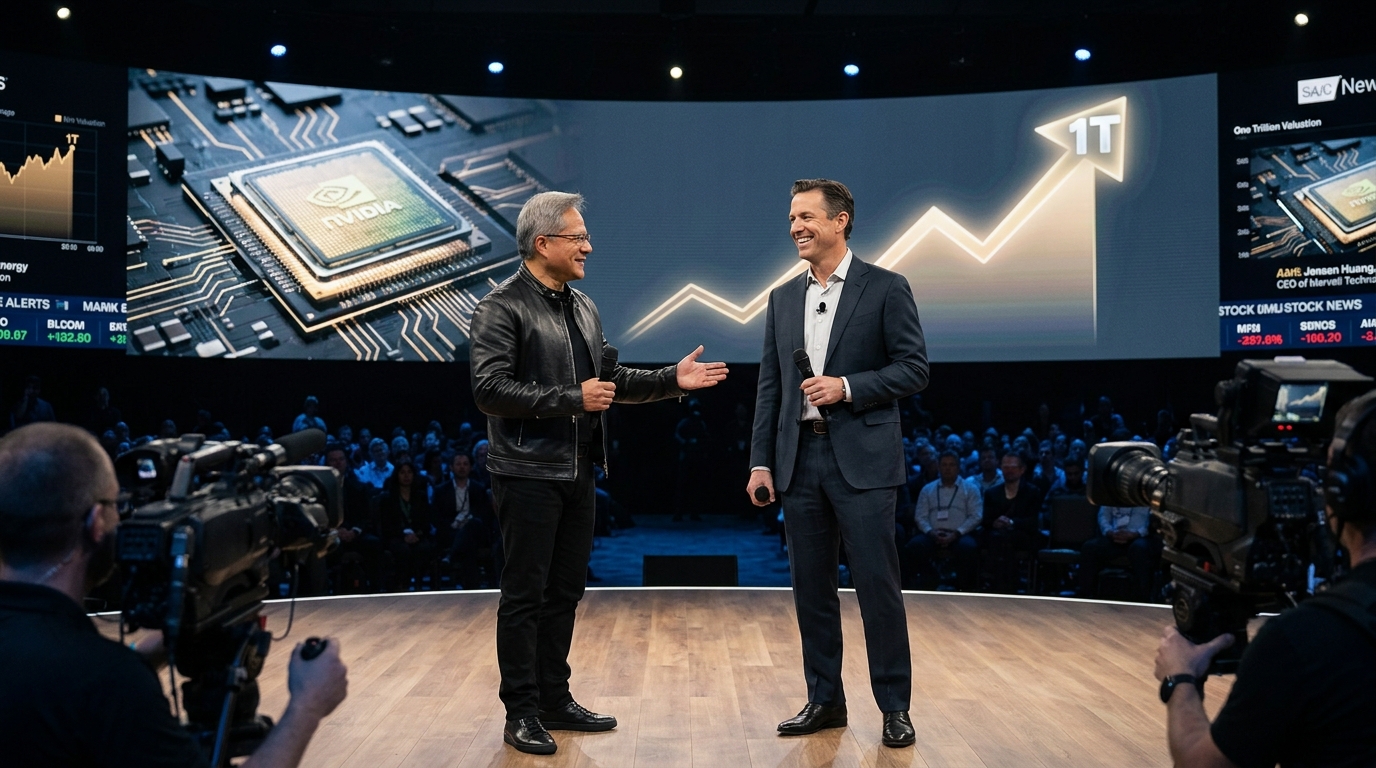

On Tuesday, June 2, Marvell Technology (NASDAQ: MRVL) posted its largest single-day gain in company history — shares surging over 32% — after Nvidia CEO Jensen Huang declared the chipmaker could reach a $1 trillion valuation. That’s not hype from a blog post. That’s the most influential person in semiconductors making a public declaration at Computex Week in Taipei, onstage with Marvell CEO Matt Murphy.

The timing wasn’t accidental.

The endorsement came just days after Marvell reported record Q1 fiscal 2027 results: revenue of $2.42 billion, up 28% year over year, driven by a 50% jump in data center revenue and AI-related bookings that management described as accelerating. Non-GAAP EPS came in at $0.80. The company then raised its full-year revenue outlook to approximately $11.5 billion — implying roughly 40% annual growth — and guided Q2 revenue to $2.7 billion, representing 35% year-over-year growth.

Why Wall Street Is Piling In

The analyst community responded with a synchronized upgrade cycle that momentum traders rarely see so cleanly. Deutsche Bank doubled its price target from $120 to $240. Stifel raised its target to $321. Roth Capital moved to $275. Raymond James lifted its target to $235. B. Riley, Wells Fargo, UBS, TD Cowen, and Oppenheimer all followed. The consensus now sits around $233, though the stock has already run past many of those levels.

Slight tangent, but it matters: Nvidia committed a $2 billion strategic investment into Marvell as part of their deepening collaboration around NVLink Fusion — Nvidia’s proprietary AI interconnect ecosystem. Marvell’s custom silicon, optical transceivers, and silicon photonics are embedded directly into that architecture, allowing hyperscalers to blend non-Nvidia custom accelerators with Nvidia’s broader AI computing stack. That’s not a partnership. That’s structural dependency.

The Numbers Behind the Story

- Q1 FY2027 Revenue: $2.42B (+28% YoY)

- Data Center Revenue Growth: +50% YoY

- Non-GAAP EPS: $0.80 (vs. $0.79 est.)

- Full-Year Revenue Guidance: ~$11.5B (~40% growth)

- FY2028 Revenue Target: $16.5B (~45% growth guided)

- YTD Stock Return: ~145% heading into Tuesday’s session

Full-year fiscal 2026 results showed revenue of $8.195 billion — a new record — up 42% from the prior year, with GAAP EPS of $3.07, up 81% year over year. The business has clearly crossed from AI story stock into AI cash machine.

Bull / Base / Bear

Bull: Marvell’s data center interconnect (DCI) business doubles by fiscal 2028 relative to fiscal 2026 levels. Custom XPU wins with hyperscalers compound. Silicon photonics via the Celestial AI and Polariton Technologies acquisitions become a structural moat. The trillion-dollar valuation Huang floated isn’t a stretch — it’s a roadmap.

Base: Growth continues to accelerate each quarter through fiscal 2027 as management guided. AI infrastructure spending holds. Margins stay near 51% gross. The stock digests its run and consolidates before the next leg.

Bear: Hyperscaler capex cycles compress. A single large customer (concentration risk is real here) pulls back custom ASIC orders. The valuation — trading near 67x earnings and 20x+ sales — leaves almost no margin for error. Any growth miss gets punished severely.

Technical Overlay

MRVL ripped from the mid-$160s to close around $280 after Tuesday’s surge, a range expansion that signals large institutional accumulation. The prior resistance near $220 becomes the first support level to watch on any pullback. The 50-day moving average is well below current levels — this is extended by any traditional measure, but extended can stay extended when the underlying thesis is this strong.

What investors should watch from here: the next earnings report (August 20, 2026), any update on bookings trajectory, and whether the $2.7B Q2 revenue guide is met or exceeded. That data point will either validate this rerating or trigger the first real test of the new support structure.

The debate isn’t whether Marvell is a good business anymore. It clearly is. The debate is whether the market has already priced in the next two years of growth in the last two months.

For informational purposes only.